Get rid bank reconciliation issues once and for all

As an NBFC the biggest challenge is reconciliation of the installments received every month. Many of the NBFC’s that we have consulted with or spoke to during our Fintech sessions or Discover sessions have shared that Reconciliation has been their biggest challenge. With a Loan book of reasonable size you are likely to have half a dozen people working on reconciliation of Bank statements and assigning the credits to the appropriate Loan accounts. Depending on the age of your lending portfolio the activity could involve

- Reconciling the credits in the bank statement with the list of NACH mandates submitted

- Checking if PDC’s are banked and reconciling the cleared cheques

- Any last minute requests for stopping mandates or stop from banking PDC’s are honoured

- Handling Over the Counter repayments

- Handling Online repayments

While the back-office operations focuses on repayments the front office staff is handling customers requests that include

- requests for the repayment mode to be swapped – Which means that NACH is swapped from one Bank to another or from NACH to PDC

- a “Stop NACH” and offers to pay Over the Counter a few days before the EMI date.

These interventions cause additional problems for the back-office operations staff during reconciliation.

Issues in reconciliation of repayments

This monthly reconciliation cycle puts a lot of operational pressure on the staff because of the various issues that tend to crop up during the course of operations. Some of the issues that we have encountered are

- NACH mandates not being executed or in the case of PDC’s, they don’t get deposited on the bank

- When customers request for swap both the mandates or the mandate and the PDC is executed

- Even when the customer requests for a stop NACH or Stop PDC and offers to pay Over the counter the NACH mandate is executed

To resolve these issues it is important to understand the way the NACH clearing process works and the technology semantics at play.

What is NACH in Bank?

The NACH or National Automated Clearing House and operated by the National Payments Council of India. All Banks who become members of NACH should have the capacity and infrastructure to process five lakh transactions per session. Each session is of 90 minutes duration.

The NACH Clearing Process

Member Banks obtain mandates either as a E-Mandate (contains a stream of data) or physical mandate from the corporates who inturn have obtained it from the customer. While physical mandates are signed by the customer E-Mandates can be verified by several authentication mechanisms like an ATM PIN or Net Banking Password etc.

All Inward files should be processed by the destination Bank within the Cut-off time, however if the destination bank is unable to process within the cut-off time then an extension can be sought and NPCI will pass on this information to the origin Banks. Origin Banks should have the capabilities to handle extensions for T+n number of days. This means that theoretically the response file can be returned to the origin bank even after thirty days from submission.

What is an NACH file format?

All origin bank submissions to NPCI for NACH clearing should be in the NACH306 file format. The NACH306 is a text file containing a header and detailed section. When the Bank originating the mandates to be processed uploads an “INPUT” file containing a list of all NACH debits that are to be processed. These debits can be on accounts held at various banks. When the destination bank receives the file it is a collection of all NACH debit mandates that it has to execute on its Core Banking System, the file is called the “INWARD” file. When the destination bank uploads the result of its processing onto the NACH system the file is the “RETURN” file.

The RETURN file contains the Settlement positions and is usually the INPUT file with the appropriate Return and Reject reason codes filled against each mandate record.

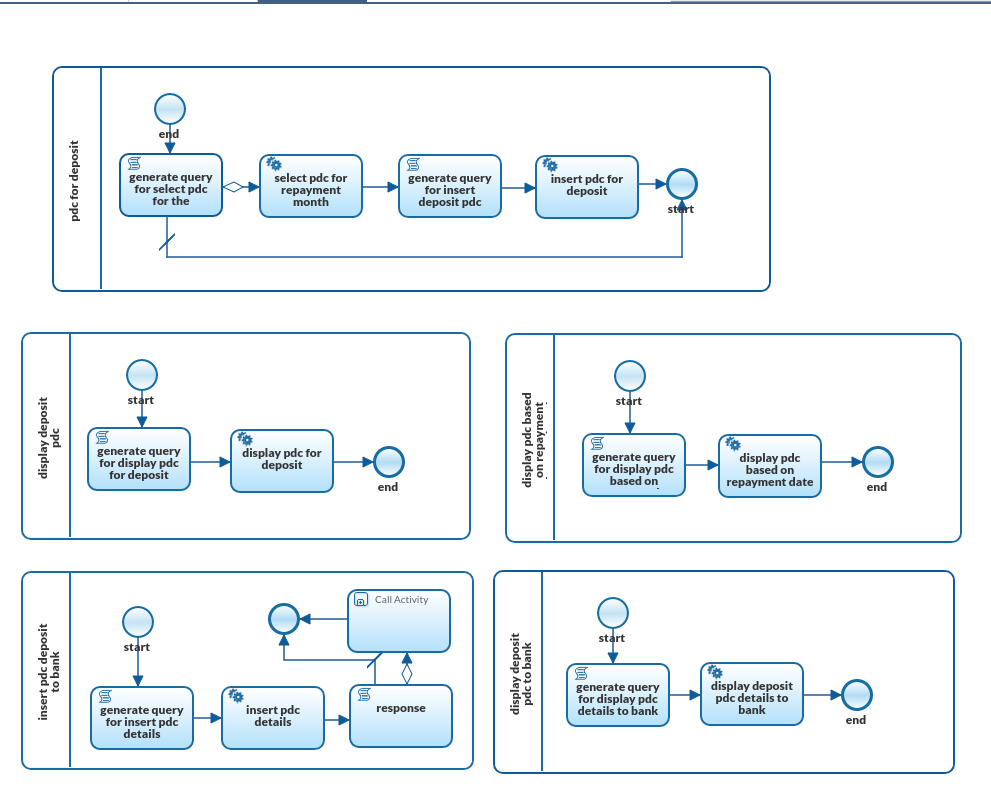

Bank Reconciliation using the ABSuite

In case of swapping requests from the customer it is unfeasible to handle it without sufficient lead time considering that the mandates have to be flagged as “STOP PRESENTATION” only after the customer has made the payment through other channels like Net Banking or through the NBFC’s portal. In case the customer hands out a cheque then there should be sufficient lead time to process it before the request for a “STOP PRESENTATION” can be met.

AB Suite checks if the payment has been made successfully before the “STOP PRESENTATION” flag can be set. In case it is not the user flagging this is appropriately warned. Once the cheque is cleared the repayment is directly assigned to the appropriate Loan Account because of the Loan Account Number having been already tagged to this cheque.

However it gets a bit complicated when an NBFC has to access clearing facilities through a bank. Because when the Bank uploads the INPUT file to the NACH system the RRN (Record Reference Number) field should contain the UMRN (Unique Mandate Reference Number).

When creating batches our experience has been that it is easier to reconcile if the batches are created Bank wise and if the number of records exceed the maximum permitted by NPCI then create the batch with Bank plus state or Bank plus city or even Bank plus Branch criteria. This way it is easier to track which banks have requested for extensions.

NBFC’s should ensure that their Loan Management system has a LAN (Loan Account Number) to UMRN mapping. One to Many relationship i.e. One Loan can have multiple UMRN’s. This is because in case of floating rate loans if the Installment amount exceeds mandate amount a fresh mandate has to be obtained. A robust mapping will ensure that when the Response file is received the LAN number can be determined by looking up the UMRN Number and the repayment can be credited to the correct Loan Account.

References

- NACH Procedural Guidelines V3.0 from NPCI